Current Price: ~ $59/share

Yield: ~ 2.02%

Rockwell Collins, Inc. designs, produces & supports communications & aviation electronics for commercial & military customers. Its products & services include cabin management systems, radar & surveillance, field support, spares & parts, among others.

Estimated WACC for the firm today is 9.76% using the Capital Asset Pricing Model and the company's recent SEC filings.

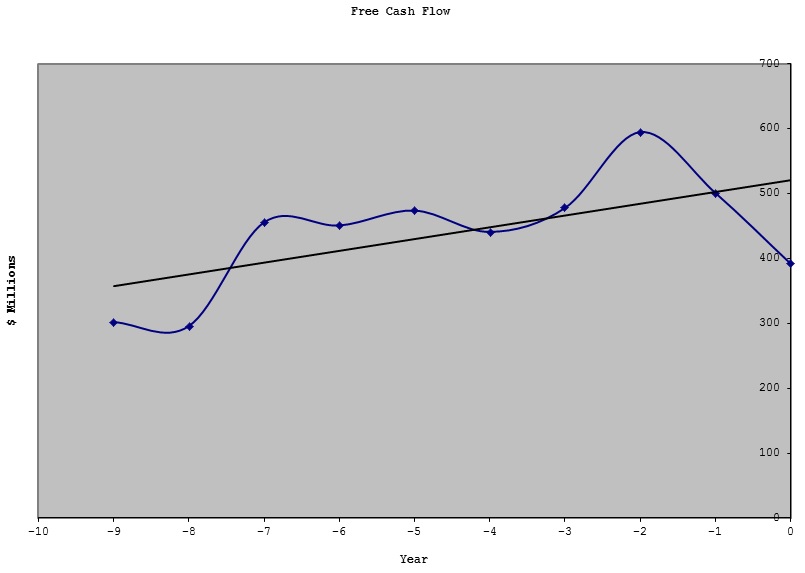

Recent free cash flows and noted growth rates:

|

Year

|

FCF $Millions

|

|

2003

|

302

|

|

2004

|

296

|

|

2005

|

456

|

|

2006

|

451

|

|

2007

|

474

|

|

2008

|

441

|

|

2009

|

478

|

|

2010

|

595

|

|

2011

|

501

|

|

2012

|

392

|

Average Annual Growth FCF: ~ 5%

CAGR FCF: ~ 3%

Consensus Forecast Industry 5-Year Growth: ~ 11% per year

Consensus Forecast Company 5-Year Growth: ~ 10% per year

Internal Growth Rate: ~ 8%

Sustainable Growth Rate: ~ 41%

Scenario 1

Average FCF (past 5 years) is $481 million

Average FCF (past 5 years) is $481 million

- Start at $481 million FCF

- Assume a 5-year growth rate in FCF of 9% per year, then no growth or 0% growth in FCF per year forever:

Discounted Cash Flow Valuation

The firm's future free cash flows, discounted at a WACC of 9.76%, give a present value for the entire firm (Debt + Equity) of $7546 million. If the firm's fair value of debt is estimated at $837 million, then the fair value of the firm's equity could be $6709 million. $6709 million / 137 million outstanding shares is approximately $49 per share and a 20% margin of safety is $39/share.

|

Year

|

FCF $Millions

|

|

0

|

481

|

|

1

|

524

|

|

2

|

571

|

|

3

|

623

|

|

4

|

679

|

|

5

|

740

|

|

Terminal Value

|

8267

|

The firm's future free cash flows, discounted at a WACC of 9.76%, give a present value for the entire firm (Debt + Equity) of $7546 million. If the firm's fair value of debt is estimated at $837 million, then the fair value of the firm's equity could be $6709 million. $6709 million / 137 million outstanding shares is approximately $49 per share and a 20% margin of safety is $39/share.

Scenario 2

All else being equal,

All else being equal,

- Assume a 5-year growth rate in FCF of 9% per year, then 2% growth in FCF per year forever:

Discounted Cash Flow Valuation

|

Year

|

FCF $Millions

|

|

0

|

481

|

|

1

|

524

|

|

2

|

571

|

|

3

|

623

|

|

4

|

679

|

|

5

|

740

|

|

Terminal Value

|

10399

|

- Present Value of the entire firm (Debt + Equity): $8884 million

- Value of Equity: $8047 million or $59/share

- 20% margin of safety is $47/share

Sources

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Hi Guys, I found a Website to perform Discounted Cash Flow Model calculations, no need to do those calculations on the Excel file anymore, check it out: http://turnkeyanalyst.com/2013/09/19/cloud-based-discounted-cash-flow-analysis-tool/

ReplyDelete